The Week in Geek™ – June 23, 2011

I’ve been way behind in posting a new Week in Geek. Thanks for your patience and continued interest! The good news is version 1.2 of my book should be out by early August (ready for the Fall semester). It continues to be made available free on the web and in low-cost print. For those interested in the publishing model, Boston College Magazine ran a story on the project titled “Textbook 2.0“.

Why Not All Earnings are Equal – Microsoft has Wal-Mart Disease Here’s an insightful article highlighting the perils of stalled growth, a concept we introduce to our freshmen in their first course in management (see the strategy section at the end of the Google Case). Citing a Conference Board study, Adam Hartung in Forbes writes: “When a company hits a growth stall, 93% of the time it will be unable to maintain even a 2% growth rate. 75% of the time we can expect it will fall into a no growth, or declining, revenue environment. And 70% of the time it will lose at least half its market capitalization.” Ouch! And Hartung argues that Microsoft is struggling to find any reliable growth prospects to move the stock needle north. To be sure, the firm is wildly profitable and mints cash. It has $29 billion in just its offshore accounts. But all that cash with lackluster growth caused the firm to begin issuing dividends last decade (pretty much unheard of for growth-oriented tech firms).

Here’s an insightful article highlighting the perils of stalled growth, a concept we introduce to our freshmen in their first course in management (see the strategy section at the end of the Google Case). Citing a Conference Board study, Adam Hartung in Forbes writes: “When a company hits a growth stall, 93% of the time it will be unable to maintain even a 2% growth rate. 75% of the time we can expect it will fall into a no growth, or declining, revenue environment. And 70% of the time it will lose at least half its market capitalization.” Ouch! And Hartung argues that Microsoft is struggling to find any reliable growth prospects to move the stock needle north. To be sure, the firm is wildly profitable and mints cash. It has $29 billion in just its offshore accounts. But all that cash with lackluster growth caused the firm to begin issuing dividends last decade (pretty much unheard of for growth-oriented tech firms).

Commentary: In its quest for new, multi-billion dollar markets Microsoft has found one in entertainment. Fueled by the Kinect (the best selling consumer electronics product of all time), the entertainment division had a nearly $2 billion Q3. But look at Bing and the results are grisly. BusinessInsider claims that Bing spends $3 for every $1 it brings in, and that losses are on a $3 billion a year run rate. Bing and Facebook have strengthened ties, with Facebook content and friends now influencing Bing results. This could be a significant alliance (Google doesn’t have access to the ‘dark web’ of content hidden behind a Facebook login, but now Microsoft does). However its unknown if adding Facebook’s punch to Bing will be enough to get users to kick the Google habit.

Microsoft’s recent purchase of Skype has lots of potential synergy. Merging Skype with Kinect would make home TV-based video calls a reality. Skype is a nice branded feature to bake into the struggling Windows Phone platform (which will soon show up on all Nokia smartphones soon, a move that cost Microsoft $1 billion). And keeping Skype’s 663 million accounts out of the hands of Google, or another rival, may also prove a savvy chess move (the prospect of a Google-owned Skype linked to Android, Gmail, and search ads may have been too much for Microsoft to stomach). Neat synergies, but profits are uncertain. Skype brought in about $860 million in revenue last year, but no profits. And Ballmer’s shop plunked down serious coin in what is now Redmond’s largest acquisition ever – $8.5 billion, about 3 times what Skype was valued at when it was spun out of eBay just 18 months earlier. With Skype inside Microsoft, the world’s largest software firm becomes the world’s largest international long distance phone company (by usage). Whether these moves are enough to help the King of the PC grow in a post-PC world remains to be seen.

Microsoft’s recent purchase of Skype has lots of potential synergy. Merging Skype with Kinect would make home TV-based video calls a reality. Skype is a nice branded feature to bake into the struggling Windows Phone platform (which will soon show up on all Nokia smartphones soon, a move that cost Microsoft $1 billion). And keeping Skype’s 663 million accounts out of the hands of Google, or another rival, may also prove a savvy chess move (the prospect of a Google-owned Skype linked to Android, Gmail, and search ads may have been too much for Microsoft to stomach). Neat synergies, but profits are uncertain. Skype brought in about $860 million in revenue last year, but no profits. And Ballmer’s shop plunked down serious coin in what is now Redmond’s largest acquisition ever – $8.5 billion, about 3 times what Skype was valued at when it was spun out of eBay just 18 months earlier. With Skype inside Microsoft, the world’s largest software firm becomes the world’s largest international long distance phone company (by usage). Whether these moves are enough to help the King of the PC grow in a post-PC world remains to be seen.

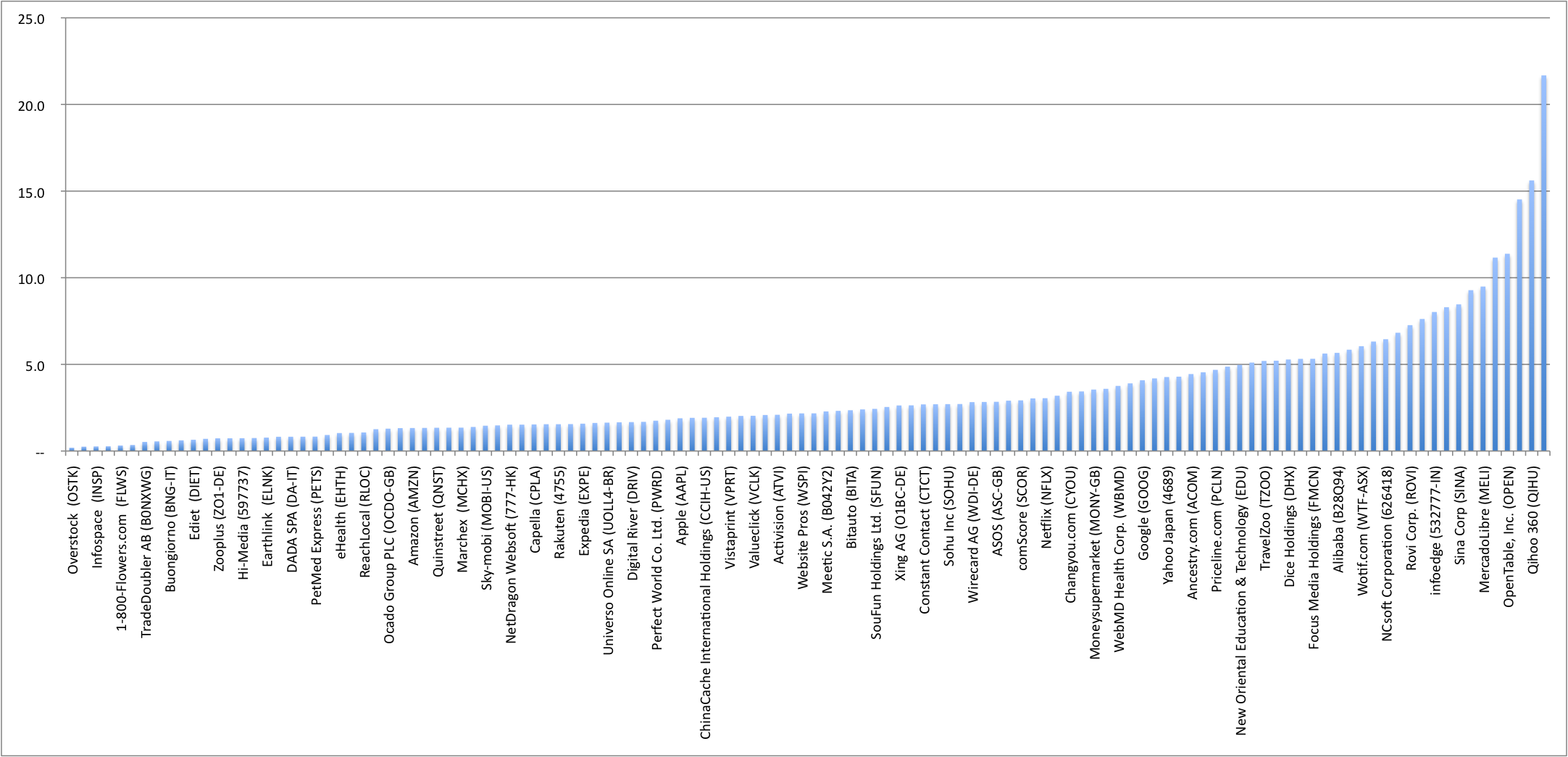

Not All Revenue is Created Equal: Key to the 10x Revenue Club

Revenue analysis was a hot topic recently and this is also a really great read. Benchmark’s Bill Gurley offers a great, example-filled listing of the key factors contributing to justifiably high valuations. I’ve also got to admit a bit of pride that so many of these themes are covered in our intro course and textbook, including factors for sustained competitive advantage, network effects, switching costs / lock-in, churn, capex, viral customer acquisition, SaaS’s revenue model & business impact, scalabilty and margins and more. While b-school bashing is often in vogue, our students should feel really good about our focus, breadth, and the validation our programs regularly receive when positively compared against what thought-leaders find important.

The Internet Bubble The Atlantic sums up an excellent infographic put out by G+, calling out a bunch of factors that suggest we’re in another bubble. The 3x accrual in Skype’s valuation over 18 months was mentioned above, but also consider LinkedIn’s brief flirtation with a $10 billion valuation despite yearly profits of $12 million (PE as of this writing – above 1800 vs. the historical 15!). The PE for Pandora (not on the infographic) is non-existent – no profits. But it had a post-IPO value of $2.6 billion. Profitless two-year-old Groupon is planning an IPO that may value the firm at $25 billion. The deals site turned down Google’s $6 billion offer earlier this year. And the site violates one of the growth tenants mentioned in the earlier article – it requires lots of human capital to scale. Groupon will soon have an editorial staff bigger than the Chicago Tribune (or any Midwest newspaper), and it’s staff of 8,000 employees (half of them sales) is several times larger than profitable and revenue-rich Facebook. A recent NY Times profile of the photo-sharing app Color paints it as a sort of Webvan-esque failure, raising a shocking $41 million in Series A funding. Color’s 38 employees inhabit a space sized for 120 that includes a custom-built half-pipe skateboard ramp. Most see Color as a failure (should have read our Network Effects chapter before the launch). By contrast, the far-more-successful Instagram raised just a bit more in total funding than Color spent on just the domain names Color.com and Colour.com, and runs with a staff of just four full timers. Anyone who lived through the dot-com bust (one of the Computer.com guys, of 2000 SuperBowl fame, was one of my students) can recognize the signs. For a laugh be sure to check out Scott Kirsner’s “Bubble? What Bubble?” look back from Jan. 2013!

The Atlantic sums up an excellent infographic put out by G+, calling out a bunch of factors that suggest we’re in another bubble. The 3x accrual in Skype’s valuation over 18 months was mentioned above, but also consider LinkedIn’s brief flirtation with a $10 billion valuation despite yearly profits of $12 million (PE as of this writing – above 1800 vs. the historical 15!). The PE for Pandora (not on the infographic) is non-existent – no profits. But it had a post-IPO value of $2.6 billion. Profitless two-year-old Groupon is planning an IPO that may value the firm at $25 billion. The deals site turned down Google’s $6 billion offer earlier this year. And the site violates one of the growth tenants mentioned in the earlier article – it requires lots of human capital to scale. Groupon will soon have an editorial staff bigger than the Chicago Tribune (or any Midwest newspaper), and it’s staff of 8,000 employees (half of them sales) is several times larger than profitable and revenue-rich Facebook. A recent NY Times profile of the photo-sharing app Color paints it as a sort of Webvan-esque failure, raising a shocking $41 million in Series A funding. Color’s 38 employees inhabit a space sized for 120 that includes a custom-built half-pipe skateboard ramp. Most see Color as a failure (should have read our Network Effects chapter before the launch). By contrast, the far-more-successful Instagram raised just a bit more in total funding than Color spent on just the domain names Color.com and Colour.com, and runs with a staff of just four full timers. Anyone who lived through the dot-com bust (one of the Computer.com guys, of 2000 SuperBowl fame, was one of my students) can recognize the signs. For a laugh be sure to check out Scott Kirsner’s “Bubble? What Bubble?” look back from Jan. 2013!

Commentary: But another side of this market shows valuations below historical averages, or that are not at all reflective of growth. Microsoft (despite concerns mentioned above) has recently traded at a paltry 9 PE. That’s about where Intel is, too. Now, Intel has threats with rivals’ power-sipping ARM-based server chips threatening its high-margin big-iron business. But both of these firms gush cash and are solidly and consistently profitable. But the most shocking is Apple – a firm that grew revenues and earnings by over 70% last year, but which is still only slightly above the historical PE of 15. Does the market really think (as one analyst puts it) that Apple won’t grow any more? So what we’ve got in the tech sector is a real anomaly. It looks like a mottled market with big patches of both bubble and value. Buckle up – tech can be wildly cyclical and it looks like we’re in the midst of the market equivalent of the Tacoma Narrows Bridge footage.

Commentary: But another side of this market shows valuations below historical averages, or that are not at all reflective of growth. Microsoft (despite concerns mentioned above) has recently traded at a paltry 9 PE. That’s about where Intel is, too. Now, Intel has threats with rivals’ power-sipping ARM-based server chips threatening its high-margin big-iron business. But both of these firms gush cash and are solidly and consistently profitable. But the most shocking is Apple – a firm that grew revenues and earnings by over 70% last year, but which is still only slightly above the historical PE of 15. Does the market really think (as one analyst puts it) that Apple won’t grow any more? So what we’ve got in the tech sector is a real anomaly. It looks like a mottled market with big patches of both bubble and value. Buckle up – tech can be wildly cyclical and it looks like we’re in the midst of the market equivalent of the Tacoma Narrows Bridge footage.

Why Content Isn’t King (and Netflix Rules) Great piece in The Atlantic that complements why we teach Netflix as one of our first strategy cases. Sure the stock is likely overvalued now, but the real point is that many predicted the firm would fail, yet Netflix has built real, durable assets for competitive advantage. “The dirty little secret of the media industry” is that content aggregators, not creators, create the most value. Think cable channels: they simply aggregate old movies, cartoons, or television but put up margins several times greater than the studios that created the content. How come? Distribution scales (fixed costs spread across multiple customers), customers have switching costs (with Netflix it’s queue, Cinematch, learning comfort, and habit-forming use). Now think about studios. Aside from sequels, do you really feel compelled to return to a Fox movie after watching one Fox hit? And what if the studio creates a superstar from their talent? A bidding war ensures that actually raises costs for the next risky, hoped-for blockbuster. No – making movies is not a good business.

Great piece in The Atlantic that complements why we teach Netflix as one of our first strategy cases. Sure the stock is likely overvalued now, but the real point is that many predicted the firm would fail, yet Netflix has built real, durable assets for competitive advantage. “The dirty little secret of the media industry” is that content aggregators, not creators, create the most value. Think cable channels: they simply aggregate old movies, cartoons, or television but put up margins several times greater than the studios that created the content. How come? Distribution scales (fixed costs spread across multiple customers), customers have switching costs (with Netflix it’s queue, Cinematch, learning comfort, and habit-forming use). Now think about studios. Aside from sequels, do you really feel compelled to return to a Fox movie after watching one Fox hit? And what if the studio creates a superstar from their talent? A bidding war ensures that actually raises costs for the next risky, hoped-for blockbuster. No – making movies is not a good business.

But the case for Netflix as distributor is even better. While cable channels serve customers through cable providers, Netflix has a direct customer relationship, which it uses to gain feedback, tailor results, and serve with award-winning service. While cable firms rank 18th of 19 industries ranked by J.D. Power, Netflix is tops in customer service and recently even beat Apple in the 528 firms listed in Brand Keys’ survey of customer loyalty.

The author of the piece, Jonathan Knee, an iBanker and Media Program director at Columbia’s B-School, echoes key points we’ve taught our students for years: “Netflix’s ability to spread the fixed costs of content, marketing, and technology across a subscriber base vastly larger than any other competitor’s is continually reinforced by superior customer service, a powerful recommendation engine, and a great, habit-forming product.” Shockingly, so many don’t see the underlying strategic dynamic. The investor Whitney Tilson wrote a “7,000 word” piece arguing for his huge bet against Netflix, and then scrambled to cover his short position after NFLX reached another new high. Wedbush analyst Michael Pachter once called the firm a “worthless piece of crap” and put a price target of $3 on NFLX (at the time trading around $11). A poster with Pachter’s photo and the “piece of crap” comment now hangs outside a kitchen at Netflix, and as of this writing NFLX trades above $250. Let’s repeat, the stock (with a PE above 70) is expensive and it’s likely that it will come down. And there are many hurdles to overcome. Cable companies are trying to throttle streaming (Netflix is now the single largest source of Internet data traffic in North America and that telcos want to meter that traffic). And negotiation for streaming content is a tough business, with some cable channels locking out Netflix during distribution windows, and others (HBO) refusing to play at all (look for even more coverage in our updated Netflix case due by August) But here’s another scenario to consider: Fortune recently argued that Microsoft should buy Netflix and make Reed Hastings the firm’s CEO. Hastings is already a Microsoft board member, Microsoft needs to strengthen its media strategy, and prior to Netflix, Hastings had already built and sold one of the 50 largest software firms. Netflix has a market cap of $13 billion and Microsoft would need to pay a premium, but Redmond is one of the few firms with the coin to pull that off. Keep that scenario in your queue.

The author of the piece, Jonathan Knee, an iBanker and Media Program director at Columbia’s B-School, echoes key points we’ve taught our students for years: “Netflix’s ability to spread the fixed costs of content, marketing, and technology across a subscriber base vastly larger than any other competitor’s is continually reinforced by superior customer service, a powerful recommendation engine, and a great, habit-forming product.” Shockingly, so many don’t see the underlying strategic dynamic. The investor Whitney Tilson wrote a “7,000 word” piece arguing for his huge bet against Netflix, and then scrambled to cover his short position after NFLX reached another new high. Wedbush analyst Michael Pachter once called the firm a “worthless piece of crap” and put a price target of $3 on NFLX (at the time trading around $11). A poster with Pachter’s photo and the “piece of crap” comment now hangs outside a kitchen at Netflix, and as of this writing NFLX trades above $250. Let’s repeat, the stock (with a PE above 70) is expensive and it’s likely that it will come down. And there are many hurdles to overcome. Cable companies are trying to throttle streaming (Netflix is now the single largest source of Internet data traffic in North America and that telcos want to meter that traffic). And negotiation for streaming content is a tough business, with some cable channels locking out Netflix during distribution windows, and others (HBO) refusing to play at all (look for even more coverage in our updated Netflix case due by August) But here’s another scenario to consider: Fortune recently argued that Microsoft should buy Netflix and make Reed Hastings the firm’s CEO. Hastings is already a Microsoft board member, Microsoft needs to strengthen its media strategy, and prior to Netflix, Hastings had already built and sold one of the 50 largest software firms. Netflix has a market cap of $13 billion and Microsoft would need to pay a premium, but Redmond is one of the few firms with the coin to pull that off. Keep that scenario in your queue.

Hackers & Thieves, A Growing Web Menace The Privacy Clearinghouse says that in 2011 we’ve had over 251 reported computer breaches involving the theft of personal information as of June, up from 234 in the same period last year. But given the headlines, you’d think the problem was much worse. Citigroup recently reported that the credit card numbers of some 200,000 customers had been compromised. A hack of Sony’s Playstation network exposed the personal records (and in some cases the credit card numbers) of about 100 million account holders. A subsequent Sony hack led to the posting of 54 megabytes of Sony’s developer source code and internal network maps of Sony BMG. Earlier this year a breach at database marketer Epsilon exposed the e-mail accounts of millions. If you were a customer of Chase, Bank of America, Best Buy, TiVo, or a handful of other firms them you almost certainly got a warning message about this last spring. Infected computers in the Massachusetts Executive Office of Labor and Workforce Development have put at risk the personal information of some 210,000 state residents. Some hacks do get a laugh – like the bogus posting on the compromised PBS Newshour site that Tupac and Biggie Smalls were alive & living in New Zealand. Others are far more serious. In March one of the most respected names in security technology, RSA (a division of EMC) was hacked. Stolen data allowed the bad guys to spoof the firm’s SecureID login systems and infiltrate RSA clients that included defense contractors Lockheed Martin, Northrop Grumman, and telecom firm L-3. In an unrelated event, what was described as a “very major breach”, the International Monetary Fund was infiltrated, with private e-mails and documents compromised. Google also went public this spring with yet another accusation of major hacking initiative within China which was apparently targeted at opponents of the Chinese government. Expect more. Says a member of the House Committee on Intelligence, the current attacks will “look like amateur hour compared to what’s coming in the next decade… We’re not moving fast enough to close the vulnerability.”

The Privacy Clearinghouse says that in 2011 we’ve had over 251 reported computer breaches involving the theft of personal information as of June, up from 234 in the same period last year. But given the headlines, you’d think the problem was much worse. Citigroup recently reported that the credit card numbers of some 200,000 customers had been compromised. A hack of Sony’s Playstation network exposed the personal records (and in some cases the credit card numbers) of about 100 million account holders. A subsequent Sony hack led to the posting of 54 megabytes of Sony’s developer source code and internal network maps of Sony BMG. Earlier this year a breach at database marketer Epsilon exposed the e-mail accounts of millions. If you were a customer of Chase, Bank of America, Best Buy, TiVo, or a handful of other firms them you almost certainly got a warning message about this last spring. Infected computers in the Massachusetts Executive Office of Labor and Workforce Development have put at risk the personal information of some 210,000 state residents. Some hacks do get a laugh – like the bogus posting on the compromised PBS Newshour site that Tupac and Biggie Smalls were alive & living in New Zealand. Others are far more serious. In March one of the most respected names in security technology, RSA (a division of EMC) was hacked. Stolen data allowed the bad guys to spoof the firm’s SecureID login systems and infiltrate RSA clients that included defense contractors Lockheed Martin, Northrop Grumman, and telecom firm L-3. In an unrelated event, what was described as a “very major breach”, the International Monetary Fund was infiltrated, with private e-mails and documents compromised. Google also went public this spring with yet another accusation of major hacking initiative within China which was apparently targeted at opponents of the Chinese government. Expect more. Says a member of the House Committee on Intelligence, the current attacks will “look like amateur hour compared to what’s coming in the next decade… We’re not moving fast enough to close the vulnerability.”

So who’s doing this hacking? A diverse group of actors. The Sony breach allegedly came from members of a hacking group that is said to be motivated more out of protest and mischief than theft-for-profit (a 19 year old was among those arrested in the case). The Boston Globe suggests that gangsters are also moving on from credit card theft to markets for stolen corporate secrets, given that widespread hacks have flooded the market with credit card numbers, causing a hundredfold drop in the street value of a stolen card. In Google’s case, it may very well be that China that went after the firm’s account holders (China has confirmed it has a cyber warfare unit but says it’s for defense only). The West hacks, too – from Stuxnet’s takedown of the Iranian enrichment program to (my personal favorite) Britain’s MI6 replacing of an Al-Qaeda bomb-making recipe with one for granny’s cupcakes. And it doesn’t help that systems are becoming more connected, more complex, and increasing the opportunities for sloppiness to slip through. For example, are you one of the 25 million Dropbox users? Well, TechCrunch reports that your files were exposed to the world “passwords optional’ for about four hours on a recent Sunday. Managers – learn the issues associated with security and make them a priority. Here’s an accessible primer – the security chapter in our textbook.

The Startup Genome An interesting, if controversial, attempt by the team behind the business accelerator BlackBox attempts to identify factors associated with successful startups. The hope is that a “Startup Genome” can be mapped in ways similar to Pandora’s mapping of the music genome. Key findings from the team’s first 67 page report are summarized in the TechCrunch post above, the full report is at http://startupgenome.cc/, complete with the requisite infographic.

An interesting, if controversial, attempt by the team behind the business accelerator BlackBox attempts to identify factors associated with successful startups. The hope is that a “Startup Genome” can be mapped in ways similar to Pandora’s mapping of the music genome. Key findings from the team’s first 67 page report are summarized in the TechCrunch post above, the full report is at http://startupgenome.cc/, complete with the requisite infographic.

{kind=link}

Making Boston More Awesome for Young Entrepreneurs The Boston Globe recently ran a collection of pieces anchored by The Road To Awesome, which examined the factors that make a region attractive to the young & talented. Curiously, the often-cited costs and government efforts seem not to have much of an impact. The piece includes a collection of essays by the young and tech-savvy with exposure to ‘tech hip’ locales in Silicon Valley & NYC, and it’s loaded with Boston College connections. The Globe’s Scott Kirsner mentions WePay and thredUp (both Bay-area ventures started by BC alumni). And the essays include contributions from BCVC ’10 winners Shahbano Imran & David Tolioupov (who also founded LocalOn in San Francisco), BC MBA ’11 Student Courtney Scrib (who attended BC’s TechTrek West & TechTrek NYC), and recent grad Andrew Boni, who helped lead BC’s IS Academy, was a participant in Valley-based TEC, and is headed to Google’s Mountain View HQ). All were former students of mine. Be sure to check out the slideshow featuring many of our alums!

The Boston Globe recently ran a collection of pieces anchored by The Road To Awesome, which examined the factors that make a region attractive to the young & talented. Curiously, the often-cited costs and government efforts seem not to have much of an impact. The piece includes a collection of essays by the young and tech-savvy with exposure to ‘tech hip’ locales in Silicon Valley & NYC, and it’s loaded with Boston College connections. The Globe’s Scott Kirsner mentions WePay and thredUp (both Bay-area ventures started by BC alumni). And the essays include contributions from BCVC ’10 winners Shahbano Imran & David Tolioupov (who also founded LocalOn in San Francisco), BC MBA ’11 Student Courtney Scrib (who attended BC’s TechTrek West & TechTrek NYC), and recent grad Andrew Boni, who helped lead BC’s IS Academy, was a participant in Valley-based TEC, and is headed to Google’s Mountain View HQ). All were former students of mine. Be sure to check out the slideshow featuring many of our alums!

I also offered my own thoughts on ‘Making Boston Awesome’ in a blog post. I can’t take credit for it, but one of my recommendations was for Boston Magazine to celebrate one young entrepreneur, in particular, and it was nice to see a Boston Magazine story on SCVNGR’s Seth Priebatsch appear a few weeks later. Now if we can just get those other requests I made come true…

Video: BC Minute – The Boston College Venture Competition For those interested in the Boston College Venture Competition, here’s a brief & very slick “BC Minute” video. And here’s a Deeper Look at the 2011 Boston College Venture Competition Finalists from Bostinnovation. Particular congrats to AddItUpp, which won an additional $10k grant as part of the selection to participate in Highland Capital Partner’s ultra-competitive Summer@Highland program, to MogloApps, which has launched their location-based game in Apple’s App Store, and to LeaseDash, which is a finalist in the MassChallenge (as a testiment to their entrepreneurial chops, know that members of this team also took the MIT $100K Executive Summary Competition with a previous idea called CityPenguin – since discontinued due to changes in the Twitter API).

For those interested in the Boston College Venture Competition, here’s a brief & very slick “BC Minute” video. And here’s a Deeper Look at the 2011 Boston College Venture Competition Finalists from Bostinnovation. Particular congrats to AddItUpp, which won an additional $10k grant as part of the selection to participate in Highland Capital Partner’s ultra-competitive Summer@Highland program, to MogloApps, which has launched their location-based game in Apple’s App Store, and to LeaseDash, which is a finalist in the MassChallenge (as a testiment to their entrepreneurial chops, know that members of this team also took the MIT $100K Executive Summary Competition with a previous idea called CityPenguin – since discontinued due to changes in the Twitter API).

Apple’s AcademiX Conference 2011

I was hugely honored to have been asked to give one of the 8 presentations at Apple’s AcademiX 2011 conference. Apple’s “TED for Ed.” was held in four locations and simulcast to an audience of 2,000. Speakers a med school dean, a law school dean, and a former ambassador – all talking about how tech has impacted their work. If you’re interested in the role of social & mobile in higher-ed, my talk was titled “Mobile & Social: Higher Ed Rocket Fuel”, and it can be streamed via the above link. It was great to see BC’s efforts given exposure!

I was hugely honored to have been asked to give one of the 8 presentations at Apple’s AcademiX 2011 conference. Apple’s “TED for Ed.” was held in four locations and simulcast to an audience of 2,000. Speakers a med school dean, a law school dean, and a former ambassador – all talking about how tech has impacted their work. If you’re interested in the role of social & mobile in higher-ed, my talk was titled “Mobile & Social: Higher Ed Rocket Fuel”, and it can be streamed via the above link. It was great to see BC’s efforts given exposure!

● ● ● ●

Oh yeah – and I’m headed to Nairobi to give a keynote talk in late August. I’d love to hear from anyone with experience / advice for a first-time Kenya traveler. I’m also very interested in researching what we at BC call “Tech for Good”, the use of information technology to empower developing regions, and want to keep this in mind as I travel, too. Any thoughts / suggestions / comments are most welcome. Thanks!