The Week in Geek™ – Jan. 3, 2012 (v. 1.3 of text is out)

Version 1.3 of “Information Systems: A Manager’s Guide to Harnessing Technology” is out! The text is meant to offer the realms of technology & business what “A Random Walk Down Wall Street” does for finance – enduring concepts wrapped around current and interesting examples. Updates will keep material current, but the book’s structure & theory will remain fairly consistent from version to version. New updates include significant work on the Netflix chapter (streaming vs. DVD, the Qwikster debacle), content on Google Plus & Motorola Mobility for the Google Chapter, Kindle & iCloud comparisons for the Moore’s Law chapter, several updates to the Facebook Chapter, and more. I hope you find the approach (two updates each year) to be the right balance offering enduring concepts alongside examples with a ‘better-than-course pack’ freshness. As always, the book is free via the browser and also available in low-cost print versions. Contact Flat World Knowledge for details. And sincerest thanks to all of you who have written with encouragement, adopted the text, and helped spread the word with colleagues. Please continue to let me know how you’re using the text, and do share with others. All the best!

Version 1.3 of “Information Systems: A Manager’s Guide to Harnessing Technology” is out! The text is meant to offer the realms of technology & business what “A Random Walk Down Wall Street” does for finance – enduring concepts wrapped around current and interesting examples. Updates will keep material current, but the book’s structure & theory will remain fairly consistent from version to version. New updates include significant work on the Netflix chapter (streaming vs. DVD, the Qwikster debacle), content on Google Plus & Motorola Mobility for the Google Chapter, Kindle & iCloud comparisons for the Moore’s Law chapter, several updates to the Facebook Chapter, and more. I hope you find the approach (two updates each year) to be the right balance offering enduring concepts alongside examples with a ‘better-than-course pack’ freshness. As always, the book is free via the browser and also available in low-cost print versions. Contact Flat World Knowledge for details. And sincerest thanks to all of you who have written with encouragement, adopted the text, and helped spread the word with colleagues. Please continue to let me know how you’re using the text, and do share with others. All the best!

Now Every Company is a Software Company David Kirkpatrick, author of the Facebook Effect, writes in Forbes: “The era of separating traditional industries and technology industries is over—and those who fail to adapt right now will soon find themselves obsolete… Regardless of industry, your company is now a software company, and pretending that it’s not spells serious peril.”

David Kirkpatrick, author of the Facebook Effect, writes in Forbes: “The era of separating traditional industries and technology industries is over—and those who fail to adapt right now will soon find themselves obsolete… Regardless of industry, your company is now a software company, and pretending that it’s not spells serious peril.”

As an example, Kirkpatrick (who also runs the excellent Techconomy conference – video excerpts here) cites Venkatesh Prasad, a senior technical leader at Ford who increasingly sees the auto giant as a firm that produces “sophisticated computers-on-wheels.” Today’s Ford cars are mobile Wi-Fi hotspots. Software manages fuel efficiency and safety systems. Sensors and software combine to automate parallel parking. Tech runs systems from navigation to entertainment. And data from smart vehicles not only feeds actionable performance data in real-time (tire pressure, breaking, and more), data fed from cars back to Ford also provides direction for engineers designing improvements for new models. Still have doubts about that ‘computer-on-wheels’ analogy? Ford is mailing out a quarter-million USB devices containing a new interface upgrade for vehincles. Now think beyond Prasad’s statements – what does this mean for today’s manager? All of a sudden issues of security, privacy, the implications of technology failure, the ability to digitally partner with others, and opportunities to create platforms for new industries – all enter the modern executive playbook. The manager who can’t think in these terms is ill-equipped for leadership in today’s environment – period.

Kenya Has Mobile Health App Fever 50% of all Kenyan banking is done on mobile phones, and many Kenyans enjoy pay-by-mobile services unavailable to most Americans. During an August visit to Nairobi I noticed that it was common to see everyone from shop keepers to cabbies swapping virtual cash via SMS text messages over the M-Pesa system offered by billion—dollar local telecom provider, Safaricom (while in Nairobi I was extremely fortunate to have had an opportunity to keynote a conference that also featured Safaricom CEO, Bob Collymore, and I’m a huge admirer of the firm).

50% of all Kenyan banking is done on mobile phones, and many Kenyans enjoy pay-by-mobile services unavailable to most Americans. During an August visit to Nairobi I noticed that it was common to see everyone from shop keepers to cabbies swapping virtual cash via SMS text messages over the M-Pesa system offered by billion—dollar local telecom provider, Safaricom (while in Nairobi I was extremely fortunate to have had an opportunity to keynote a conference that also featured Safaricom CEO, Bob Collymore, and I’m a huge admirer of the firm).

But Kenya-tech isn’t just about banking – Technology Review points out that Kenya is paving the way in other areas, including potentially high-impact mobile health apps. MedAfrica from Nairobi-based Shimba Technologies (co-founder Steve Mutinda Kyalo is pictured) offers critical tools to a nation where only 7,000 doctors serve a population of 40 million. The MedAfrica platform offers up real-time health information, aggregating multiple sources such as first-aid treatment and health alerts from local hospitals. The firm also plans to tap into data from NGOs and the national Ministry of Health to support coverage of disease outbreaks and exposing counterfeit drugs. And customers can use the app to find medical practitioners in their area. MedAfrica hopes to keep services free and ad supported, with for-fee premium services offered in the future. The app is currently being downloaded at a rate of about 1,000 new users each day, with 60% reporting active use. And a partnership with Safaricom, Kenya’s leading mobile provider, will help bring the effort to the nation’s 25 million mobile phone subscribers.

Safaricom is also working with the startup Call-a-Doc, which allows the telecom firm’s 18 million mobile subscribers to make advice calls to doctors for about two cents a minute. Another effort, Mpedigree, is rolling out an SMS-based service at health-care centers to provide a way to check serial numbers on drugs so that counterfeit meds aren’t used. And don’t forget Boston-based Sproxil (where one of my former students works), also a key player in combating drug counterfeiting. Beyond Kenya, Africa Aid offers MDNet – a system that has logged over a million free voice calls (texting is also supported) linking patients with a network of 1,900 physicians in Ghana. Moore’s Law fuels cheap cell phones and just might extend life spans by providing the equivalent of a doc in the pocket of millions that are currently under-served.

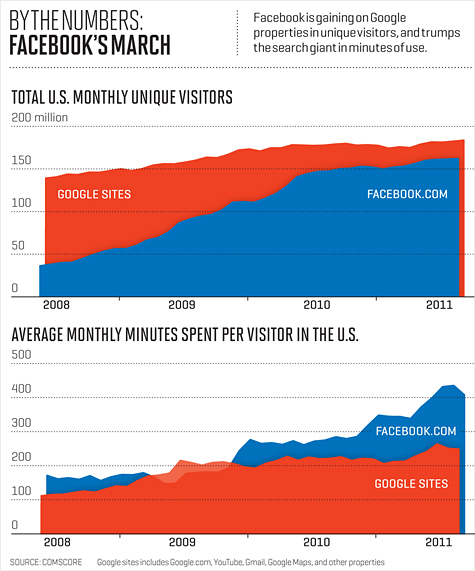

Facebook vs. Google Social networking is now the world’s No. 1 online activity, occupying 20% of online time. Four years ago, that figure was just 6%. And the war over social is fodder for a recent Fortune cover story on Facebook vs. Google (bonus at link above: scroll for video of Google exec Marissa Mayer on privacy, & Facebook’s Mark Zuckerberg topping the ’40 under 40’). Both firms are surging, and each is building a rock-solid set of strategic assets. Says Fortune “rarely has there been a battle as competitive as the raging war between the web’s wonder twins.”

Social networking is now the world’s No. 1 online activity, occupying 20% of online time. Four years ago, that figure was just 6%. And the war over social is fodder for a recent Fortune cover story on Facebook vs. Google (bonus at link above: scroll for video of Google exec Marissa Mayer on privacy, & Facebook’s Mark Zuckerberg topping the ’40 under 40’). Both firms are surging, and each is building a rock-solid set of strategic assets. Says Fortune “rarely has there been a battle as competitive as the raging war between the web’s wonder twins.”

The overwhelming majority of profits from both firms come from ad dollars. Google is a behemoth- taking in some 41% of the U.S. online ad market. Facebook’s estimated $4.3 billion in ’11 revenues are less than half the $9.6 billion Google brought in last quarter, and Larry Page’s firm is estimated to snare $38 billion in ‘11. But Facebook’s revenues more than doubled in size in 2011, while Google’s should grow by 30%. That’s slower growth, but in dollar terms, Google is still growing by adding more than an entire Facebook’s-worth of revenues in 2011. These are remarkable numbers given the horrendous global recession, but at some point all markets mature and as one analyst says, it’s highly unlikely that either firm “could grow by the billions that investors expect… without engaging directly and stealing market share from the other.”

Google search is a rifle-scope targeting ads when you’re on the hunt for information. But Facebook is a microscope exposing who you are and what you’re up to. If we opt into Facebook’s deep integration with other apps, we tell Facebook what we’re doing – listening to tracks on Spotify, watching videos on Netflix, using RunKeeper to train for that 10k – and all of that is advertising gold. Even worse for Google – most of the content on Facebook is in the ‘dark web’, un-crawlable by Google’s search spiders because it lies protected behind a Facebook login. Developers dig how Facebook helps spread the viral love of their new offerings, and with each new adoption, it’s an opportunity for Facebook to reveal even more of you under that microscope. It’s worth noting that Facebook’s login credentials are becoming a real catalyst for web innovation. One might bail on a new site if it required a new password, but might try a site if it accepts the Facebook login.

The importance of social isn’t a new realization for Google – but nearly all of the firm’s prior efforts were dismal failures. You’ve likely never used (or perhaps even heard of) Google’s Orkut unless you were in Iran or Brazil – two of the only places where it dominated. Google Buzz was a poorly-tested, privacy-exposing failure that prompted an FTC investigation. And the much-touted Google Wave bombed – pulled within months of launch.

But the June launch of Google+ is described by Fortune as “a network that cloned much of what people like about Facebook and eliminated much of what they hate about [it]”. Google+ users get profile pages, games, photos, status updates, and a +1 that mimics Facebook’s “like”. But Google also offered features to manage privacy & share updates only with “circles” of contacts that you curate (e.g. posts for groups like friends, family, co-workers, or the public). And while Facebook charges app developers 30% of revenue, the Google vig is just 5%.

Google’s approach to innovation has been widely criticized, but Larry Page sought to lead the effort top-down, and create accountability for social. “Page moved his office and much of the executive suite to the building where the Google+ team was sequestered”, and he tied a significant portion of employee bonuses to metrics tracking the success of social. Page even made demands on design – pushing simplicity like one-button photo uploads. Says Google’s other co-founder Sergey Brin, the firm still wants to be flexible enough that a thousand flowers can bloom, but “once they do bloom, you want to put together a coherent bouquet.” Google+ has been growing like gangbusters. Already at 60+ million one bullish report suggests it’ll be at 400 million users by next year if the firm can keep up with the current pace of adding 625,000 users a day.

Facebook didn’t stand still. Shortly after the debut of Google+, Zuckerberg flicked a switch on the pink neon “lockdown” sign at Facebook’s HQ, signaling the troops to “work around the clock” pushing Facebook’s rollout forward and cutting off some of the edge some saw in Google+. By September, Facebook had rolled out a group-curation tool to counter Google Circles, plus a whole slew of enhancements designed to embed Facebook at the center of the social web. This shows the challenge of competition on the social front – technology can be easily matched, so unless it comes with a way to create or counteract advantages of user base (e.g. network effects, data) then upstarts will struggle to displace incumbents. Google has a vast ad network serving ads from sites ranging from BusinessWeek to small-time blogs, lots of cash, and killer platforms for integrating & distributing social (search, Gmail, YouTube, Android, and more). Whether or not this is enough to create an enduring reason to spend more time outside the Facebook social monopoly remains to be seen. But Google may not need to win outright –a strong second-place showing in social could still mean more data for better ad targeting and improved services throughout the firm’s properties.

The battle is also playing out in a talent war. Over 10% of Facebook employees are so-called xooglers (ex-Google employees), including four of Facebook’s top eleven executives, as well as the Google engineer considered the father of Google+’s Circles feature. Still, Google remains one of the most sought-after employers, and the firm has added nearly as many employees in the recent quarter (2,600) as Facebook has on its entire staff. Facebook will soon lose a key weapon in the talent war – the chance to get a slice of pre-IPO equity and the possibility of liquidity-event coin. Once Facebook goes public, the firm’s stock price will be subject to market whims just like Google (which, incidentally, is up about 7.5 fold in the seven and a half years since going public). Hot-money heat-seekers may follow the next big IPO candidate (Twitter? Xooglers are about 13% of their workforce).

Facebook vs. Google is a very fun place to research and write about. Those interested in diving in with more details can see the January 2012 release of the Facebook and Google chapters in my textbook.

Why Netflix Customers Who Haven’t Bailed Probably Won’t

For those thinking Netflix has backed off plans on its full-steam-ahead streaming future, check out CEO Reed Hasting’s comments from last month’s UBS Media Conference: “We’re going to try to not hurt [the DVD-by-mail business], but we’re not putting a lot of time and energy into doing anything particular around it… We’re focused on, how do we take advantage of this incredible global streaming opportunity.” Even if you used to get both DVDs and streaming videos from Netflix, the company will only tell you about its streaming plan in its “come back!” emails, as far as Netflix marketing goes, it’s as if the DVD biz doesn’t exist. And the firm no longer allows you to ‘gift’ someone a DVD subscription – gifts are streaming-only. Hastings has even called DVDs “Old fogey discs”. Sure DVDs are a billion-dollar-a-year business servicing millions of subscribers, but its days are numbered.

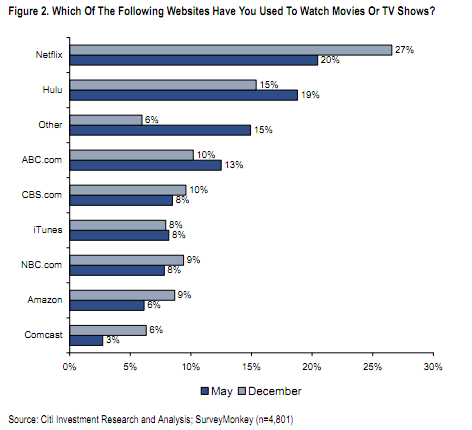

It’s been a tough year for Netflix. The firm’s stock price plummeted from $300 to below $80, and it’s customer service rank (which regularly topped leading surveys) has plummeted. The most recent Forsee index ranked rival Amazon as number one (although it’s worth noting the survey compares a firm’s entire e-commerce offering, so it’s not just a streaming-to-streaming comparison). Some 900,000 Netflix customers bailed the prior quarter. Those numbers are grim, but a Citigroup survey of customers remaining with the firm suggests most will stay and that growth should be looking up.

57% of current customers reported they were either “extremely satisfied” or “very satisfied” with Netflix. ‘Extremely satisfied’ customers are down to 18%, from 50% in May. But the survey also reveals that most of the firm’s customers don’t see many other decent options. Only 15% of Netflix customers report using Hulu to view movies or TV shows – no other site cracks 10%. These results echo a similar study by PC World showing that even with the price hike, Netflix was still the best value in both video streaming and DVD-by-mail.

That latter stat also made it into the January ’11 update of the Netflix chapter in my book. The update also includes a chart comparing the DVD-by-mail and streaming businesses – I hope you find it to be a good teaching aid for fueling class discussion around atoms-to-bits shifts and technology disruption.

Bonus: those following Netflix will likely find talks by the firm’s engineering honcho (who tweets at @adrianco) to be fascinating. The blog post “How Netflix gets out of the way of innovation”, offers a number of gems below – they’d likely generate useful class discussion as well as insights for the entrepreneur. Nuggets from the blog post cover “how did we keep making big strategic moves, from DVD to streaming, from Datacenter to Public Cloud, from USA only to International, all in very short timescales with a fairly small team of engineers.” Other highlights:

- “Netflix is now one of the largest sites that runs almost entirely on public cloud infrastructure. We have become a poster child for how to build an architecture that takes full advantage of the Amazon Web Services cloud.” Recent problems are blamed on ‘Roman Riding’ – still having a foot in old data-center architecture while migrating to the cloud.

- “It’s the things you don’t do that make the difference. You don’t add innovation to a company culture, you get out of its way.”

- “Who has junior engineers, graduate hires and interns writing code? We don’t. We find that engineers who cost twice as much are far more than twice as productive, and need much less management overhead.”

- “Reducing management overhead is a key enabler for an innovative culture. Engineers who don’t need to be managed are worth paying extra for.”

- The firm doesn’t have an architecture review board or centralized coding standards. Instead, engineers are free and responsible for figuring it out for themselves. Peer pressure helps keep quality high.

- On the cloud “AWS takes about 5 minutes to allocate 100 servers, it takes longer than that just to boot Linux on them.”

- “We don’t pay bonuses. We don’t have grades other than senior engineer, manager, director, VP. We don’t count the hours or the vacation days, we say “take some”. Once a year we revise everyone’s salary to their peers and current market rate – based on what we are paying now to hire the best people we can find.”

- “We also have what sounds like a crazy stock option plan that grants options every month, vests the same day, and they last 10 years even if you leave Netflix.”

Those interested in engineering and public cloud topics might also hunt out Adrian’s talks on on YouTube.

Last bit of Netflix news (of particular interest to my students who are visiting with our alumni connections in the Xbox group next week), a new version of streaming over Xbox 360 allows users to use voice and gestures to control the app.