Facebook IPO Analysis & More – The Week in Geek™ – May 24, 2012

Fun Facts: Smart phones made up 36% of Q1 global phone shipments. 13% of US consumers own a tablet. Which is the fastest growing tech ever?

What is Facebook Worth? Since many Week in Geek readers are either studying or teaching the Facebook chapter, I offer some extensive analysis of the IPO, plus current & future outlook for the firm. At IPO, Facebook priced at $38. Just two days before trading, the firm upped by 25% the number of shares offered. Facebook raised some $16 billion, the IPO initially valued the firm at over $104 billion, and the offering clocked in as the biggest technology IPO of all time and the third largest IPO in US History (trailing only Visa & GM).

Since many Week in Geek readers are either studying or teaching the Facebook chapter, I offer some extensive analysis of the IPO, plus current & future outlook for the firm. At IPO, Facebook priced at $38. Just two days before trading, the firm upped by 25% the number of shares offered. Facebook raised some $16 billion, the IPO initially valued the firm at over $104 billion, and the offering clocked in as the biggest technology IPO of all time and the third largest IPO in US History (trailing only Visa & GM).

$38 is the price big investors got the stock for. Trading for the masses opened at a bit north of $42 and closed around $38.23. In one respect this is good for Facebook. The firm raises its money at the $38 share price, so a big first day ‘pop’ would have meant that public markets valued $FB higher than the price iBankers set, and money would have been “left on the table”. But the price slipped and by the second day of trading shares had already fallen below the issue price. Hype and uncertainty often conspire to make IPOs bad investments. Google is actually an exception. Initially undervalued by Wall Street and for roughly a month post-issue hovering at near its IPO price, Google became a growth monster. Even though early PEs were high and shares were up more than 2x by the end of its first year as a public firm, earnings kept going up and to the right, initially expensive shares grew into (and beyond) lofty expectations, and shares quintupled in in less than four years. If you bought GOOG any time in its first year and held the shares, you’ve trounced the market.

Time for some analysis:

Comparing Numbers: FB, GOOG, and AAPL: Is Facebook the next Google? So far Facebook’s growth looks sketchy. Facebook Q1 growth rate was 45%, down from 55% the prior quarter, which was down again from triple digit growth the prior quarter still. Still-growing Google now trades at 13x 2013 EPS. Facebook IPO’d at a nosebleed 65x 2013 EPS. While Facebook’s market cap is about half of Google’s, in the business where Facebook & Google most closely compete (display ads), Google’s business is growing faster. Google also has more cash than Facebook has revenue. Facebook’s free cash flow is actually negative (blame the cost to build data centers – you’ve gotta put all those photos somewhere). Apple shares offer a less fair comparison, but consider that Apple trades at 10x estimated 2013 EPS, the firm’s revenues have consistently grown in the 70% range, and the Apple has a decade-long, rock-solid track record of blockbuster product introductions with no sign of a stumble in sight. By these measures the Facebook issue price seem like a whole lot of speculation.

Outlook & Opportunity: What about upside? Facebook is lean – it has very small sales force (in the prior year Google hired about 8,000 employees, or about 2.5x Facebook’s total headcount at IPO. Now that the firm has billions in new capital, expect Facebook to go on a hiring spree. Many of these new employees will be sales reps tasked with bringing in new business.

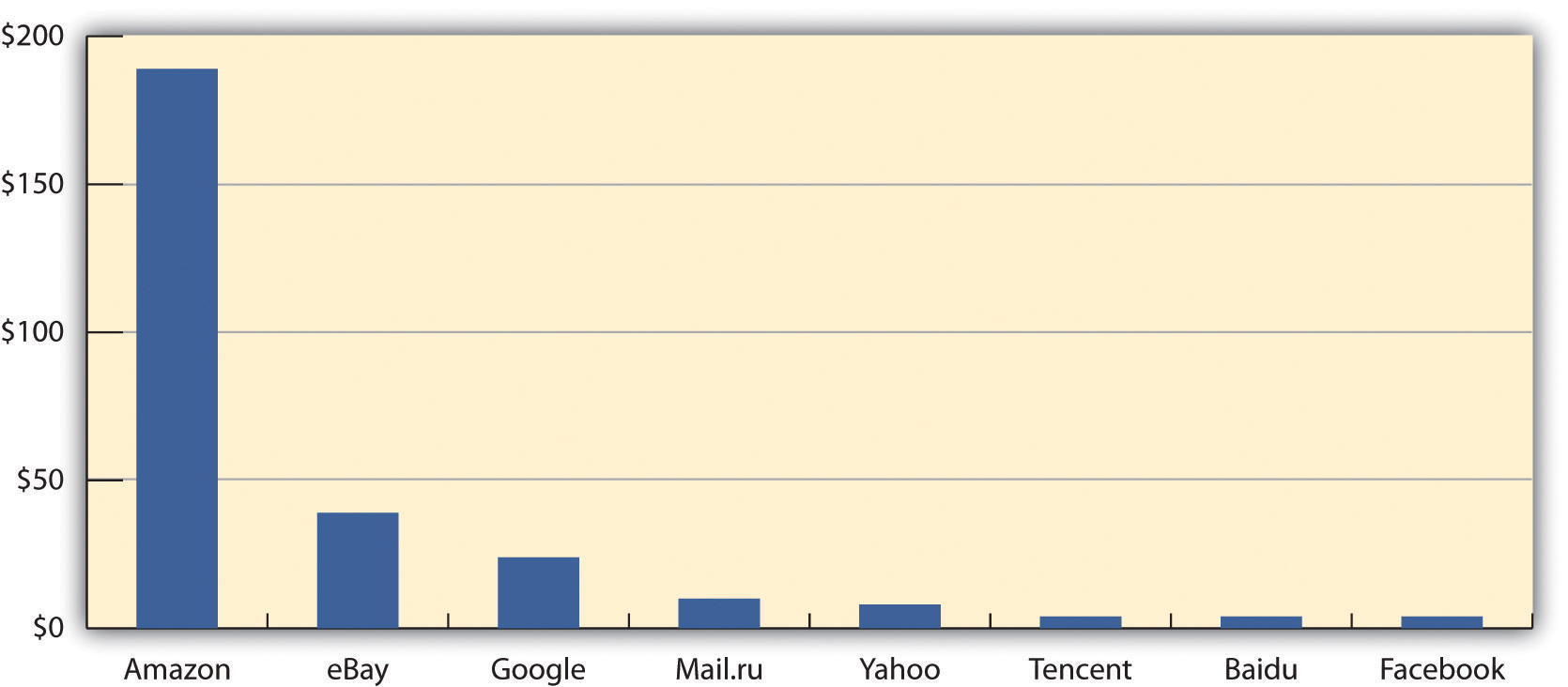

An Ad Network More Valuable than Google’s?: Most coverage of Facebook’s opportunities for expansion has been terrible, so let’s look at this in more depth. One easy opportunity is the ad network. Google earns about 30% of its revenue from ads that run on websites Google doesn’t own (it targets ads, collects coin from advertisers, and splits the take with website operators, see the blue area on the chart above). Facebook doesn’t have an ad network yet, but turning one on is technically trivial. Ramping up the rollout so it’s not a privacy debacle and doesn’t lead to a deluge of scare headlines will be the tough part. Analysis that shows Facebook ads perform far less effectively than Google ads is all true (see the ARPU or avg. revenue per user chart below, as well as “The Hunt vs. The Hike” metaphor from our course material). But a Facebook ad network could actually perform better than Google’s. Google targets ads on other websites based largely on keywords found on that page + browser history. Facebook can do all this, but can also add in data from your social activity, your personal profile, and other insight that lies in the “dark web” that Google can’t see. Here’s a simple equation: AdSense <; AdSense + FB social + FB profile + other data from the FB dark web.

Mobile – Not a Good Near-term Payout: Facebook will also roll out mobile ads. Mobile represents about 40% of Facebook use, but brings in virtually zero in revenue. Offering ads on mobile will be easy – getting users to pay attention to them is the tough part. Google should bring in about $10/Android user, but targeting ads on search is way easier than social (again see the The Hunt vs. The Hike‘ in the Facebook chapter). Not wanting to lose mobile is one reason Facebook spent $1 billion for Instagram, a 18 month old firm with 13 employees.

Keeping Advertisers Satisfied: There will also be a lot of tinkering with ad formats, and there is great upside potential. Facebook took in only $3.2 billion in advertising last year (for ref, Google’s revenues were about 12 times that), and many top-tier advertisers have $1 billion+ overall ad budgets. But some suggest Internet advertising will always be valued less expensively than offline counterparts, and that unit prices are likely to drop (Michael Wolf’s piece in Technology Review is especially pessimistic). Others also question the value in social ads. In the days before the Facebook IPO, GM pulled a $10 million account with Facebook saying Facebook ads don’t work (Note that GM is also pulling ads for the 2013 SuperBowl).

Longer Bets – Payments & Television: Longer term two of the more interesting potential areas for Facebook growth are payments and television. Linking credit cards to everything from splitting a restaurant bill to renting a video seems like a Facebook natural (Zynga’s early value of $10 billion was based largely on the sale of virtual goods over Facebook). And as the Week in Geek has argued before, Facebook almost certainly wants to play a starring role in your living room, making the TV a platform for all sorts of activity: video chat, serving targeted ads, social entertainment recommendations, games, and all sorts of commerce. Navigating the tensions of bandwidth capping cable guys, channel owners, and hardware firms keen to build their own platform, will also be tough. But Zuck has Reed Hastings on his board – as much as he’s been derided this past year, no one has built a further reaching platform with consumer electronics firms than Netflix.

Longer Bets – Payments & Television: Longer term two of the more interesting potential areas for Facebook growth are payments and television. Linking credit cards to everything from splitting a restaurant bill to renting a video seems like a Facebook natural (Zynga’s early value of $10 billion was based largely on the sale of virtual goods over Facebook). And as the Week in Geek has argued before, Facebook almost certainly wants to play a starring role in your living room, making the TV a platform for all sorts of activity: video chat, serving targeted ads, social entertainment recommendations, games, and all sorts of commerce. Navigating the tensions of bandwidth capping cable guys, channel owners, and hardware firms keen to build their own platform, will also be tough. But Zuck has Reed Hastings on his board – as much as he’s been derided this past year, no one has built a further reaching platform with consumer electronics firms than Netflix.

Global Growth: Nice, but Lower ARPU: All these new products will be far more important in the mid term than Facebook’s expanding user base. The firm is already approaching 1 billion users, and those users will only be valuable once their income, standard of living, and attractiveness to advertisers goes up. A growing user base in the developing world is a great human-empowerment story. But right now the ARPU (average revenue per user) of notably poorer new Facebook users isn’t going to have anywhere near the impact we saw from the firm’s prior user growth. By the way, for ideas on how to up ARPU for low-income, developing nation mobile users, see the amazing work being done by Jana a firm we visited on a Boston TechTrek last semester.

Morgan Stanley Criticized for Facebook IPO Wall Street’s reigning champ of the tech IPO is Morgan Stanley. The firm not only led Facebook’s debut, it was also lead underwriter on LinkedIn, Zynga and Groupon. Since the beginning of 2010, Morgan Stanley’s largely Valley-based tech banking team has generated $1.2 billion in fees. That’s a quarter billion dollars more than #2 player JPMorgan Chase. These tech deals generated 13% of Morgan’s overall i-banking fees, vs. 7% at JPMorgan and 9% at Goldman.

Wall Street’s reigning champ of the tech IPO is Morgan Stanley. The firm not only led Facebook’s debut, it was also lead underwriter on LinkedIn, Zynga and Groupon. Since the beginning of 2010, Morgan Stanley’s largely Valley-based tech banking team has generated $1.2 billion in fees. That’s a quarter billion dollars more than #2 player JPMorgan Chase. These tech deals generated 13% of Morgan’s overall i-banking fees, vs. 7% at JPMorgan and 9% at Goldman.

Critics say Morgan Stanley mismanaged the Facebook offering, by either signing off on a price that was too high, or agreeing to sell too many shares in the deal. But let’s be fair – Facebook was oversubscribed and it was by far the most eagerly anticipated IPO of the decade. Just about all pundits predicted a substantial pop. With Zuck controlling voting rights he can take a long view, he’s been clear he’s not going to chase quarterly performance figures, and everyone getting into FB knew this’d be the case.

I wonder if the auction market of OpenIPO by iBanking legend Bill Hambrecht (shown here in an earlier meeting with my students & holding the “tombstone” from taking Apple public) may have helped. Hambrecht thinks Facebook should have offered users a stake, first. The institutions that are in on the IPO often look to flip for quick profits during the pop. Many of those investors also report quarterly results, so there’s little incentive to hang on to a stock during a correction. But if the issue price was crowdsourced via auction, there may have been a greater chance that long-view investors willing to buy & hold would have gotten in, reducing the allocation to the flippers & short-term skittish.

I wonder if the auction market of OpenIPO by iBanking legend Bill Hambrecht (shown here in an earlier meeting with my students & holding the “tombstone” from taking Apple public) may have helped. Hambrecht thinks Facebook should have offered users a stake, first. The institutions that are in on the IPO often look to flip for quick profits during the pop. Many of those investors also report quarterly results, so there’s little incentive to hang on to a stock during a correction. But if the issue price was crowdsourced via auction, there may have been a greater chance that long-view investors willing to buy & hold would have gotten in, reducing the allocation to the flippers & short-term skittish.

Several agencies are also “looking into whether Morgan Stanley and other bankers broke rules when the firms’ analysts cut their earnings forecasts on Facebook just days before the IPO” and are examining whether Morgan provided advice to some but not all of its clients (which would violate provisions against “selective disclosure” if this did indeed happen).

If Morgan looks bad, so does the Nasdaq, which experienced a series of software glitches resulting in the “unexpected delay at the start of trading, missing trade execution messages and, at one point, orders that were filled by hand”. When Facebook bumped up the shares issued, it created larger than expected allocations among institutions, leaving Nasdaq unprepared for a high number of order cancellations that came in while the exchange was trying to calculate the FB opening price. Finance guys, we’ve got a number of examples where software rules your world, for better or worse. Also remember events two months ago where “exchange operator BATS Global Markets was forced to withdraw its initial public offering on its own market after being plagued by software errors.”

Add to all of this the circus leading up to events, which included Michael Pachter of Wedbush Securities issuing a public scolding of Zuckerberg for wearing a hoodie during the roadshow. Sorry, Pachter, but you don’t have the cred to make that kind of call-out. He was the guy who said that Netflix at $11 was headed for $3 (the stock spent the next five years steadily climbing ‘til it was above $300, and even post Qwikster debacle, NFLX still trades at about 25 times Pachter’s target).

Etsy Seeks Scale without Losing Its ‘Street Fair’ Aesthetic Etsy is a juggernaut. Last year sales grew 67% and the firm pulled in north of $525 million. Etsy hosts more than 800,000 “stores” that collectively sell over 13 million different items. Etsy generates more than 39 million unique visitors a month (US traffic ranks ahead of Target, Groupon, or Best Buy). Etsy is also the most “pinned” site on Pinterest. The firm makes money on a 20 cents an item listing fee, and takes a 3.5% cut of an item’s sale price. Driven by network effects, the site now seeks to maintain its quirky feel and dedication to the small artisan, craftsperson, and vintage clothing vendor without succumbing to the soul-stealing lure of mass marketers. Huge thanks to BC alum & former student Chris Cosentino, payments guru at Etsy, for hosting our students and arranging for a master-class on-site with CEO Chad Dickerson.

Etsy is a juggernaut. Last year sales grew 67% and the firm pulled in north of $525 million. Etsy hosts more than 800,000 “stores” that collectively sell over 13 million different items. Etsy generates more than 39 million unique visitors a month (US traffic ranks ahead of Target, Groupon, or Best Buy). Etsy is also the most “pinned” site on Pinterest. The firm makes money on a 20 cents an item listing fee, and takes a 3.5% cut of an item’s sale price. Driven by network effects, the site now seeks to maintain its quirky feel and dedication to the small artisan, craftsperson, and vintage clothing vendor without succumbing to the soul-stealing lure of mass marketers. Huge thanks to BC alum & former student Chris Cosentino, payments guru at Etsy, for hosting our students and arranging for a master-class on-site with CEO Chad Dickerson.

PayPal Rival WePay Raises Another $10 Million Congratulations are in order for BCVC co-founder and TechTrek Alumnus Bill Clerico, and his Boston College co-founder Rich Aberman, on raising a $10 million Series B round for their payments startup, WePay. WePay’s early VCs, August Capital and Highland Capital Partners are joined in the Series B round by Seattle’s Ignition Partners. Early angels include PayPal co-founder Max Levchin & super-angels Ron Conway & Dave McClure, and the firm has raised a total of roughly $19.5 million. An alum of the elite Y-Combinator accelerator program, WePay has emerged as a legitimate and more nimble PayPal competitor, known for great service and dead-simple products. WePay tools focus on four use cases: selling products online, selling tickets, accepting donations and sending bills to request payments (the latter is great for clubs, PTAs, splitting up roommate & vacation bills, group gifts, and more). WePay also allows merchants to create their own online stores and embed stores in their own sites.

Congratulations are in order for BCVC co-founder and TechTrek Alumnus Bill Clerico, and his Boston College co-founder Rich Aberman, on raising a $10 million Series B round for their payments startup, WePay. WePay’s early VCs, August Capital and Highland Capital Partners are joined in the Series B round by Seattle’s Ignition Partners. Early angels include PayPal co-founder Max Levchin & super-angels Ron Conway & Dave McClure, and the firm has raised a total of roughly $19.5 million. An alum of the elite Y-Combinator accelerator program, WePay has emerged as a legitimate and more nimble PayPal competitor, known for great service and dead-simple products. WePay tools focus on four use cases: selling products online, selling tickets, accepting donations and sending bills to request payments (the latter is great for clubs, PTAs, splitting up roommate & vacation bills, group gifts, and more). WePay also allows merchants to create their own online stores and embed stores in their own sites.

◆ ◆ ◆

Also some brief BC-related updates:

- The 2012 winner of the Boston College Venture Competition is Namib Beetle Design, a firm that is developing a biomimicry technology to extract water from the atmosphere. Team includes Miguel Galvez, BC ’12, who is also a TechStars Fellow. [See coverage in Bostinno & The Heights]

- The first winner of BC SEED’s Social Entrepreneurship competition is Maji Bottles, a firm that has already sold enough water bottles to give over 100 people clean drinking water for life. [See coverage in Bostinno #1 & Bostinno #2 ]

- BusinessWeek has ranked the Boston College Information Systems Department #4 in the U.S., the highest ranking of any of the Carroll School’s departments [Interactive Table].

- BC IS Prof. Sam Ransbotham was recently interviewed by MIT’s Sloan Management Review. Our own ‘Big Data’ expert will be offering a new undergrad business analytics course this Fall.

- TechTrek East (Boston & NYC) is a finalist for the MITX Award for “Best Contribution to Innovation by a University”. Come out to the awards ceremony on June 12.

And a reminder – if you’re a Boston College alumnus in the Boston (East) or Silicon Valley / Bay Area (West) and you’re not a member of the BC Technology Council, then you’re really missing out. The May dinner featured a student entrepreneurship showcase, student presentations on tech & entrepreneurship innovation at BC, networking, and a phenomenal talk by Nikesh Arora (BC Alum), Chief Business Officer at Google. To get on BCTC’s events mailing list simply e-mail bctc@bc.edu. I hope to see you at future events!